Estimated read time: 5-6 minutes

Inflation has cooled since its spike to 8% in 2022. But with the inflation rate still hovering around 3% as of summer 2024 according to Investopedia, consumer goods prices remain high. The inflationary surge of the last few years has stretched consumer budgets thin and forced many to rely on their credit cards more than ever to cover everyday expenses.

As a result, the Federal Reserve Bank of New York reported consumer credit card debt reached a historic high of $1.14 trillion in Q2 of 2024. Adding to the strain, annual percentage rates (APRs) on credit cards have skyrocketed to an average of 27.64%, Forbes reported. And the Consumer Financial Protection Bureau reports that consumers are facing all-time high APR margins, meaning credit card companies charge a much higher interest rate on balances compared to the cost they incur to borrow money themselves.

For consumers, high APR margins translate to more expensive debt that too many people simply can't repay, resulting in what the Federal Reserve Bank of St. Louis stated are the highest delinquency rates since 2011. This situation underscores the dire importance of exploring options that can reduce the financial strain.

The cost of high-interest credit card debt

Credit cards can be a useful and rewarding financial tool when used strategically. But as people turn to high-interest credit cards to manage the gap between income and expenses, they're finding themselves trapped in a cycle of debt, with high APRs making it more difficult to pay off balances that quickly balloon into unmanageable sums.

Credit card APRs can vary widely, ranging from around 10% to as high as 30% or more. These rates might not seem like a big deal when you're only making minimum payments, but they can lead to significant financial consequences over time. The higher your interest rate, the more you'll pay in interest, and the longer it will take to pay off your balance.

This high-cost borrowing can have far-reaching consequences for your financial health. Not only does it compound how much you owe and take longer to pay off, but it can also:

- Strain your budget and make it impossible to save for your financial goals.

- Cause financial stress and delinquency. Over time, the accumulation of interest can become so burdensome that it feels impossible to make a dent in your principal balance.

- Lower your credit score so it's more difficult and expensive to obtain credit in the future.

- Impact your health, creating anxiety and even physical health issues.

- Cause reliance on credit. In severe cases, individuals may find themselves relying on more credit to make ends meet, further deepening the cycle of debt.

Here are some examples of how high-interest credit card debt can harshly affect individuals:

The impact of carrying a balance on a high-APR credit card

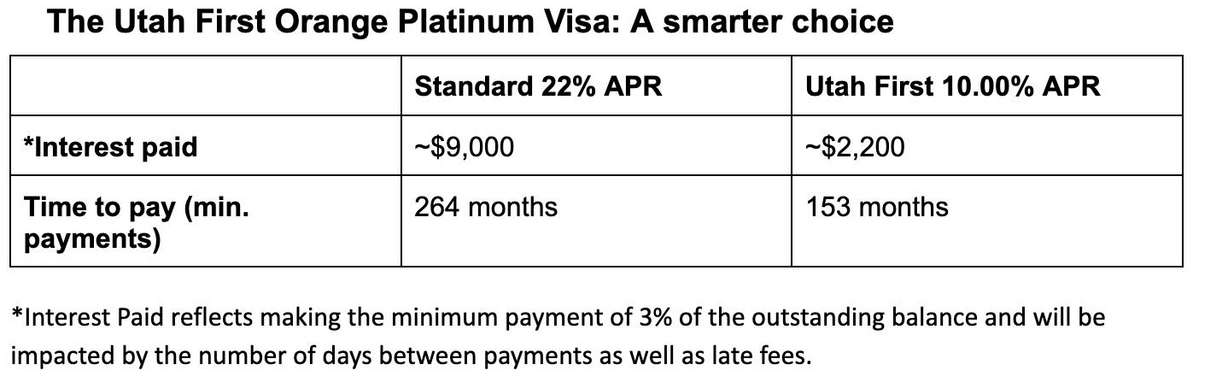

Let's say you have a credit card with an interest rate of 22%, and you're carrying a balance of $6,000. The credit card company requires you to make a monthly minimum payment. If you don't pay more than that each month, you'd be paying off that debt for 264 months, nearly 22 years! By that time, you will have paid around $9,000 in interest alone.

Now, let's say you carried the same balance on lower-rate credit card like the Utah First Orange Platinum Visa. This card offers a highly competitive interest rate of just 10%, which can significantly reduce the amount of interest you'll pay over time and shorten the payoff period.

Loan Balance: $6,000

Interest Rate: 10.00%

Monthly Payment: 3% of the balance (approximately $180)

With the lower interest rate, you could pay off your balance in about half the time of the higher-rate card. More importantly, you'd pay less than $3,000 in interest, saving you nearly $6,000.

Refinancing your existing credit card debt

If you're currently carrying a balance on a credit card with a high rate, it might be time to consider refinancing your balance with a lower-rate card. Many people don't realize that credit card refinancing is an option, but it's a smart financial move that can help you reap big-time savings.

When you refinance, you transfer your existing balance from a high-interest card to a new card with a lower interest rate. This process can often be done easily online, and it's a straightforward way to reduce your interest payments. However, not all credit cards are created equal, so it's important to choose a card that offers a competitive rate and favorable terms.

The Utah First Orange Platinum Visa provides excellent value, helping users save at a 10% fixed APR with no annual fee while offering easy balance transfers, one reward point for every $1 spent and flexible redemption options.

Compare your rate and take control of your debt

As inflation and other economic factors continue to drive up the cost of living, and with credit card interest rates at record highs, it's critical to take control of your finances now by securing a lower interest rate. Every percentage point matters; the difference between a 24% interest rate and a 10% rate can add up to thousands of dollars in savings over time.

Take the time to review your current credit card situation, compare rates and consider whether refinancing with a lower-rate card could be the right move for you.

If you're paying more than 10%, transfer your balance to the Utah First Orange Platinum Visa and start saving money today.